Your savings rate is the most important figure in personal finance. It is the same as the profit in the business world. We are all aware that all companies must earn profits. This is the only way campaigns can grow and prosper. However, most people don't realize that profit is just as important for people!

Last week Michael Kitces published an interesting article that argues spending rates matter more than saving rates. He writes:

Most households are always trying to save because at the end of the month there is no money left to save in the first place. The main problem is not the low rate of savings, but the too high rate of expenditure. Saving and spending are two sides of the same coin. However, Kitses has his own point of view.

Saving Rate vs. Spending Rate

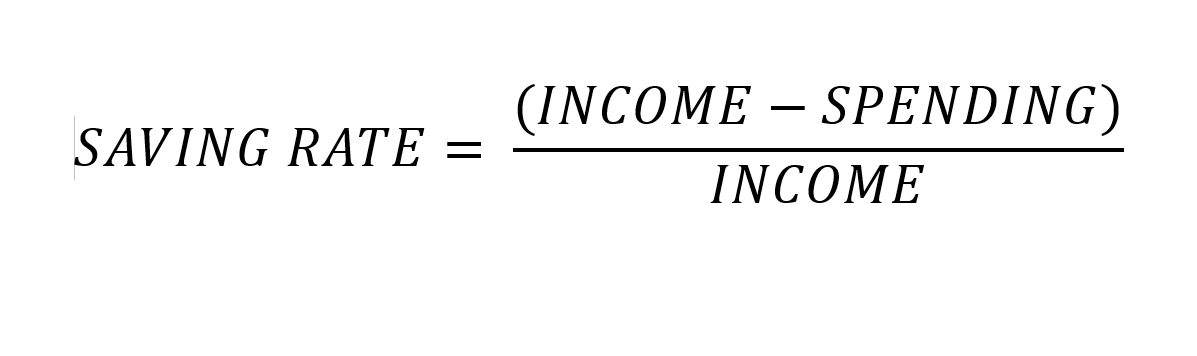

Your savings rate is calculated by dividing your profit (your income minus your expenses) by your income.

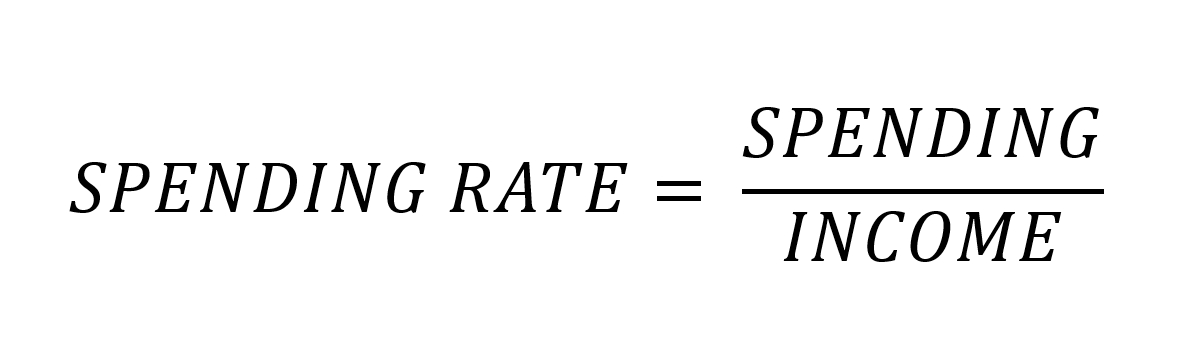

Your spending rate is calculated by dividing your spending by your income.

The equations above show that the savings rate and the expenditure rate are opposite to each other. If you have a 70% spending rate, then you have a 30% savings rate. If you have a 10% savings rate, then you have a 90% spending rate.

Kitses argues that it is very important to pay attention to the costs. He also believes that saving is just a side effect. Your income and spending are two numbers that you can control in the equation. Saving is a by-product. This is a secondary factor. This is a very important observation.

Saving as Side Effect

Over the past few years, people have been convinced that they should not make debt relief their main financial goal and there are reasons to do so.

Everybody knows the cases where people only lived to get out of debt. But as soon as they are free of debt, they immediately return to bad financial habits. The same is with people who set a goal to become financially independent. Those who achieve their goal realize that this is not the panacea they had hoped for.

Sometimes financial independence and debt reduction should be treated side effects. They are by-products of other more important financial decisions. You will get out of debt if you cut your expenses and increase your income. It will happen without your purpose. And if you clearly understand your personal mission, then you will achieve financial independence - if FI is aligned with that particular mission. (FI doesn't fit every goal in life.)

Thanks to the Kitches, we should realize that saving is a side effect. "The real key to saving is not “saving” itself, but establishing reasonable spending principles," he writes. He's absolutely right.

Your income and your expenses are two variables in the fundamental wealth equation that you control. However, you can’t control your savings directly. These increases or decreases depending on two other factors.

- If you increase your income, your savings rate rises. If your income decreases, your saving rate falls.

- If you reduce your spending, your saving rate rises. If you increase your spending, your saving rate falls.

If you want to save more, you should adjust your expenses (or your income). For example, to set aside 10%, you need to spend 90% of your income instead of 95%.

Control What You Can Control

I like the transition from a “savings rate” to “spending rate”, because it focuses on what you can really do to improve your situation. You can't directly improve the side effects. To do this, you need to make adjustments to the primary reasons (this is your income and your spending). After that you will control your spending much better.

In order to earn more money, you have to do whatever you can:

- Get education.

- Work harder and smarter.

- However, opportunities to increase income don’t appear often, but opportunities to reduce spending appear every day.

How to reduce your spendings?

- Reduce the cost of housing. The biggest monthly expenditure for the average American family is housing. Finding cheaper housing is the most effective way to reduce your spending rate.

- Transport is the second largest expense in the average American budget. In this case, spending can be reduced by riding by bus or bike to work.

- Reduce recurring monthly expenses. Surely most of us have a list of subscriptions and regular payments such as Spotify, Pandora, Apple Music, etc. These bills accumulate and become a huge cash flow.

So, does spending rate mean more than saving rate? Do I agree? Yes and no.

You can’t argue that the spending rate is more important than the savings rate or vice versa. In fact, they are the same thing, but from different sides. However, we agree that savings are a side effect, not a major factor. The fact is that a person can directly influence his spending. So can he influence his borrowings. To help you do it wise, saving your money and time, we've designed the COMPACOM.com website. Compare the companies or apply online.

You are about to post a question on compacom.com:

Any comments or reviews made on this website are only individual opinions of the readers and followers of the website. The website and its authors team are not responsible, nor will be held liable, for anything anyone says or writes in the comments. Further, the author is not liable for its’ readers’ statements nor the laws which they may break in the USA or their state through their comments’ content, implication, and intent.