Is it Better to Save Money or Pay Off Debt?

Any kind of debt can cause a lot of trouble, especially when it interferes with the accumulation of funds. In this case, many people are faced with a choice: pay off the debt in full and save nothing or leave some savings but remain in debt.

At the same time, few people know that there is an opportunity to find an alternative and combine debt repayment and save money. It is this balance that is very important in order to feel confident and calm. People who manage to combine these two aspects clearly have more stable financial health.

If your budget does not quite allow you to combine savings and paying off debts, you need to prioritize. To do this, you need to know the advantages of both aspects and draw up an individual plan for distributing your finances.

How many Americans are in debt?

Financial experts say that almost 80% of Americans deal with debt. Accordingly, 8 out of 10 Americans are faced with the issues of paying off debts and saving money. We can say that the debt hole has already become a way of life for Americans, and they have practically no idea how to get out of it.

Average Debt Amount by Type

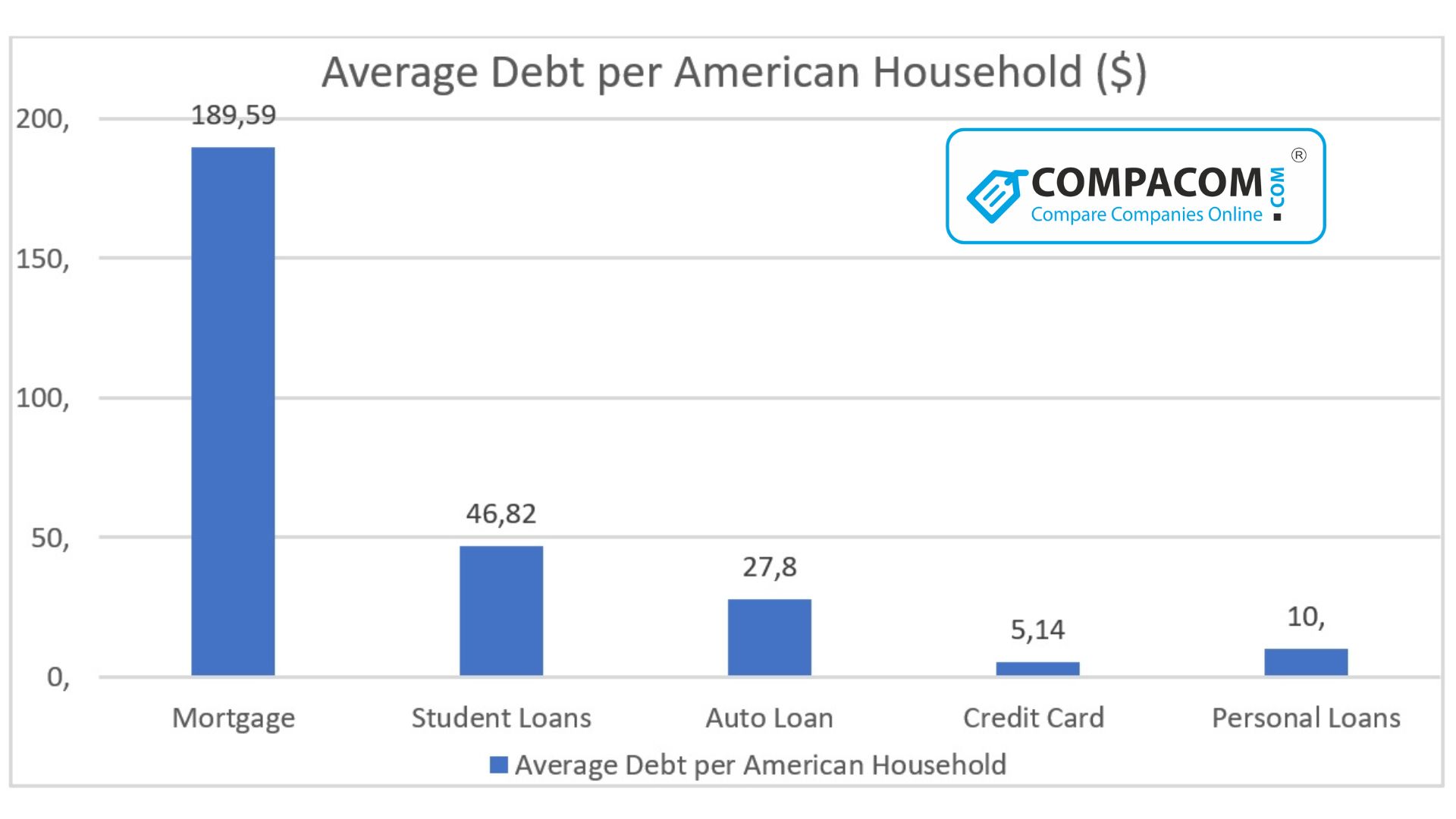

The average debt in the United States is $38,000, excluding mortgages. Americans have a total debt of $14 trillion, most of which is mortgages. The amount of mortgage long is equal to 9.4 trillion dollars which per family is $189.586. The second largest is student debt which is $46,822 for a household, then car debt which is $27,804, and the credit card debt of an American family average $5,135. The others include personal loans or small payday loans.

Why you should pay off debt

Considering that 1/5 of all Americans spend half of their income paying off their debts, there are several good reasons to pay them off as soon as possible.

- Once you pay off your debts, you can turn your attention to saving your income. The faster you pay off your debts, the less money you will spend, since the term of payment of debts affects the interest rate. The timely payment of debts also allows you to achieve a better credit history and get guaranteed approval for $5,000 - $35,000 personal loans, for instance.

- Getting out of debt has a positive effect on your mental health, especially if you want to deal with financial services in the future and need a good credit score. In this case, you should pay all your attention to this particular aspect of life and try to pay off all your debts as soon as possible.

- If you conditionally spend $3,000 on a credit card with an interest of 17 percent, and you pay only the minimum amount every month, you will spend much more than you originally planned by $510 (17 percent). Given that the minimum payment is 4 percent, you will spend many years paying off the debt that will be accumulated over many years.

- Speaking of paying off debts, all people choose for themselves different ways of paying off. Thus, some people prefer to deal with the highest-interest debts first, while others prefer to pay off the cheapest debts first to keep them from becoming even more expensive. The most effective way is to make several individual plans and decide which one will work in your case. As soon as you deal with all your debts, you can put the allocated amount into savings.

When to prioritize debt repayment

In the event that you have debts with high-interest rates, it is better to deal with them immediately, as they are the most costly and take a lot of money from the family budget. Once you deal with expensive debt, the number of monthly expenses will be significantly reduced.

- In order to start paying off debts, take into account a few points:

- Look at your monthly income and calculate if any of them can be cut;

- Calculate your actual income after paying all bills, taxes, and food;

- Having a final budget, calculate the maximum amount you can allocate to pay off debts.

Making such a plan allows you to prioritize. The best thing to do is to make paying off your debts a top priority. Tara Alderete, director of education and community at Money Management International, says that in almost all cases paying off your debts should be your top priority, but of course, there are exceptions. “If you already have adequate savings in your emergency fund, you may want to focus on quickly eliminating debt. However, if you find yourself making only minimum payments on debts with extremely high-interest rates, those debts may be causing you to lose money and preventing you from achieving your overall financial goals, and you may want to focus on paying off that costly debt.”

Tara argues that in any budgeting it is worth taking into account your priority expenses first of all, after which you could allocate funds to pay off all your debts and at the same time even be able to save money. If you are faced with the choice of saving money and paying off taxable debt, it is better to pay off the debt anyway, as the tax loss is likely to be lower than the interest rate on the debt anyway.

How to Get Out Of Debt Fast

In case your debt issues outweigh your savings issues, here are some tips:

- Review your expenses. At the stage when you analyze your expenses, pay attention to whether something can be cut. Whether you need to go out for dinners that often and whether you need all the subscriptions to services that you sometimes don’t even use. If you start small, you can save big in the long run.

- Go beyond your budget. At the moment when you analyze your income and expenses, try to squeeze out the maximum free money. Conditionally, if you can set aside a maximum of $500, try to allocate 400 of them for debts, and set aside 100.

- Consider ways to get low or no rated debt. For example, you may consider refinancing your debts or consolidating them. This makes especially sense in the case of student debts if their interest rate is 8 percent or more. The meaning of such an action is to reduce the amount of all interest and save in the long run.

Pros of prioritizing savings

At the same time, there are several distinct advantages to making savings a priority firstly.

- Savings can save you from future debt in case you have unforeseen financial difficulties.

- You can start achieving your goals now instead of waiting to pay off all your debts.

- More time to take advantage of interest accrual.

Probably the last point is the most popular. The sooner you start saving money in a savings account, the more you can get from the interest on this amount.

Each year can make a significant difference when saving money. Let's say you start putting $5,500 a year into your retirement account at age 25. If you continue to do this until age 65 at 7 percent interest, you will have $1.17 million available. But if you make it to age 35, that income will almost halve to $556,000.

Saving money can also help achieve goals such as saving for children's education, buying a house, and so on.

Of course, savings help you feel calmer and more confident, as you always feel that you have additional funds. For example, you have lost your job or need to move urgently. It is savings that will allow you to refrain from a credit or a loan with a high credit rate which is why saving money should be your priority too.

When to make a saving priority

There are a number of points that make people start saving money first, and then pay off their debts:

- Opportunity to have access to an employer 401(k) match program;

- Very low-interest rates on debt;

- No emergency savings.

A certified financial planner and founder of Pearl Planning, a financial planning and wealth management practice in Dexter, Mich named Melissa Joy says it makes sense to look at savings first if you have a credit or debit card with a low-interest rate.

The second case is when your job gives you access to a retirement savings plan. If you do not use this plan, then you will actually lose free money. If you delay putting money into a pension fund until you pay off all your debts, then you will lose the most important resource - time.

But of course, the most important advantage to start saving money as early as possible is the creation of a financial cushion in case of emergency expenses. This will allow you to feel more confident and calmer in case some situation in life requires urgent cash spending.

First, create an emergency fund

While paying off your debts may be your priority, you should consider setting up an emergency account. Even a small amount set aside once a month can make a significant contribution to your future and situations where you may urgently need a certain amount. Losing a job or needing urgent repairs can throw you off the rails if you don't have an emergency fund set aside. Without such funds, the need for credit or loans with a high-interest rate may increase significantly, which will subsequently cost you much more.

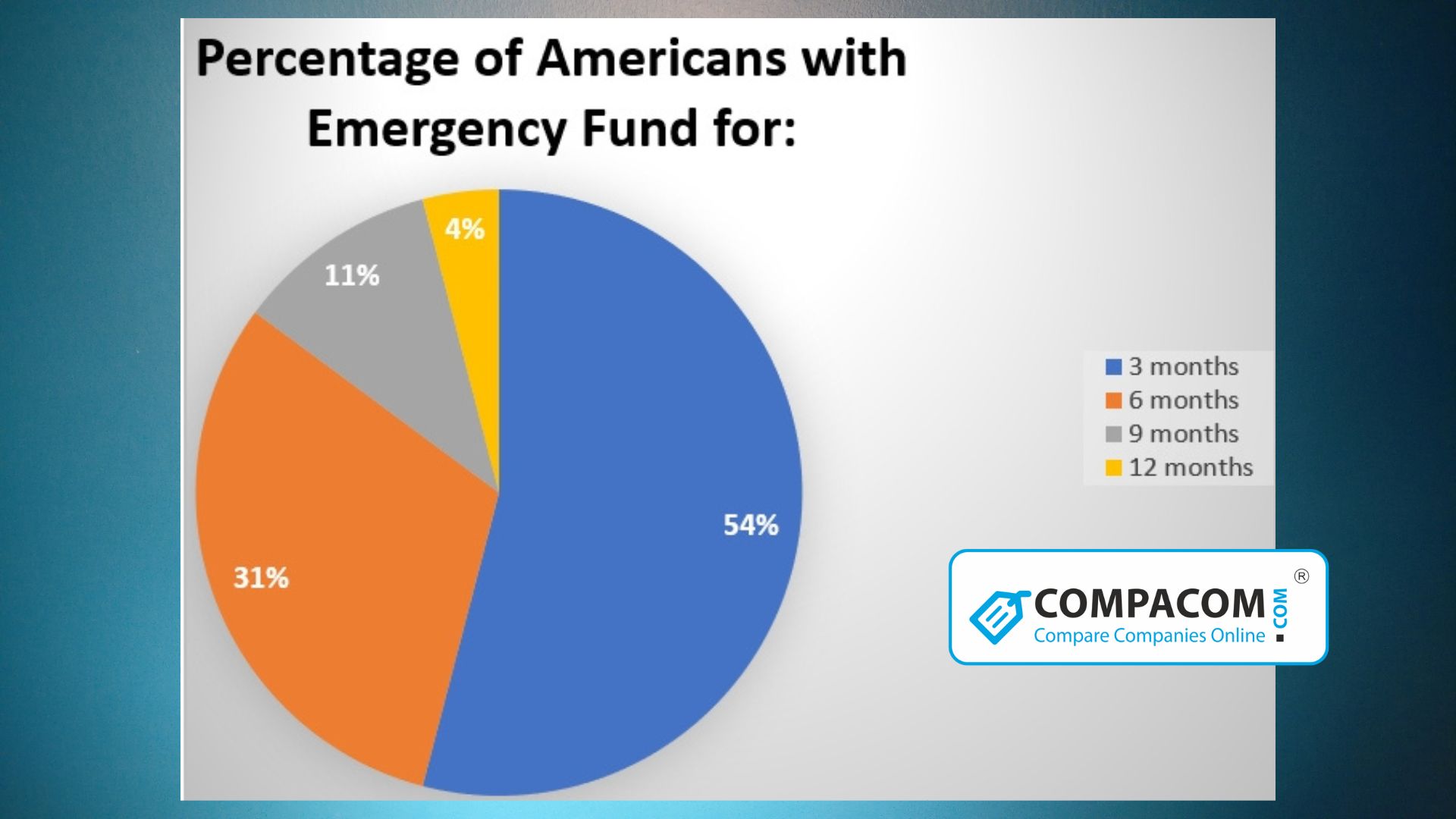

How many Americans have an emergency fund for 3, 9, or 12 months of expenses?

Unfortunately, not all Americans have such accounts with savings, which can be enough for 3, 6, or 12 months. About 26 percent have no savings at all.

Ideally, for a single person, the amount of savings is the funds that will be enough for 6 months of living, however, for people with debts, this is not always realistic. In this case, the best option would be to set aside funds for at least 3 months, because having at least some funds in case of emergency is better than having nothing. If you set aside even a little money for three months, you will already feel much calmer and will be able to focus on further savings after you pay off your debts.

When saving money, it is a good idea to open a savings fund with a high interest in order to increase the amount of your savings even when you are busy paying off debts. At the same time, if you're focusing on savings, be sure to pay off at least a small portion of your debt so that the interest rate doesn't start to rise even faster and your credit history doesn't deteriorate.

How much to save

A CFP with Abacus Planning Group, Inc. in Columbia, S.C. named Aaron Graham recommends that you start saving at least enough for one month's living. "There is no excuse for not saving for these emergencies," Graham says. "It's not a question of if they will happen, but when; plan accordingly."

Ideally, your savings should be enough for you to last between 3 and 6 months. Some experts even argue that you should have enough funds in your account for the year ahead. In order to choose the best bank for yourself with suitable conditions, you need to try to store money in several banks at once.

Can you pay off debt and save?

As mentioned above, it is possible to combine the accumulation of funds and the payment of debts. For this you need to follow a few tips:

- First, you need to calculate your budget. Look at how much money you are spending on debt repayment and whether you can somehow save these costs by refinancing or debt consolidation. This decision allows you to cut your interest rate and spend more money on the debt itself.

- Next, you need to calculate what costs you can save and what costs can be completely eliminated. Once you have calculated everything, you need to decide how much of the allocated money you can give to pay off debts, and how much to save. For example, you managed to set aside $400, $250 of which will go towards paying off debt and $150 towards savings. So at the end of the year, you will have 1800 money set aside. No matter how much you put aside if you make money work, it will definitely give you financial independence and freedom in the future.

The bottom line

If you decide to postpone the payment of the debt and save all funds, this will lead to an increase in the interest rate and a deterioration in your credit history. If you do not save at all and spend everything on paying off debts, then you can lose a large amount due to the time spent. That is why the best solution would be to combine both.

You are about to post a question on compacom.com:

Any comments or reviews made on this website are only individual opinions of the readers and followers of the website. The website and its authors team are not responsible, nor will be held liable, for anything anyone says or writes in the comments. Further, the author is not liable for its’ readers’ statements nor the laws which they may break in the USA or their state through their comments’ content, implication, and intent.